$60k a Year is How Much an Hour? (Full Financial Breakdown)

Are you wondering how much is $60,000 a year per hour? We’ve got you covered with all the details

Author: Kari Lorz – Certified Financial Education Instructor

You’re looking for a new job, but you’re not sure if $60,000 is enough to support your family. After all, the cost of living is on the rise. But how much is $60,000 a year per hour? And can you live on it?

It can be hard to know how your salary translates into a working monthly budget. But don’t worry, we’ve got you covered. In this article, we’ll break down what $60,000 per year really means for you, your budget, and for your family.

This post may contain affiliate links. If you make a purchase, I may make a commission at no cost to you. Please read my full disclosure for more info

- Are you wondering how much is $60,000 a year per hour? We've got you covered with all the details

- $60k a year is how much an hour (short answer)

- If you make a $60k salary, how much is that after federal and state taxes?

- What do retirement contributions do to my take-home pay?

- How much does insurance take from my $60,000 annual salary?

- How to live on $60k a year

- How should I budget a 60k salary?

- Can you live off of $60k a year?

- Jobs that make $60,000 a year

- What about bonuses?

- $65,000 a year is how much an hour?

- At the end of the day

$60k a year is how much an hour (short answer)

- Let’s say you work the traditional 40 hr workweek:

- $60,000 / 52 weeks a year = $1,153.85 a week / 40 hours = $28.85 an hour

- $60,000 / 52 weeks a year = $1,153.85 a week / 40 hours = $28.85 an hour

- If you work 50 hrs a week (which would be more typical for a salaried worker):

- $60,000 / 52 weeks a year = $1,153.85 a week / 50 hrs = $23.08 an hour

How much is $60,000 a year in monthly pay?

- $60,000 / 12 months = $5,000 gross pay

How much is $60,000 a year in bi-weekly pay?

- $60,000 / 26 pay periods = $2,308 gross pay

$60k is how much a week?

- $60,000 / 52 weeks = $1,154 gross pay

$60,000 is how much a day?

If you work 40 hours a week, 8 hours a day = $231 a day when working.

$60k a year is how much an hour?

Remember you are salaried! That means you get paid that same even when you work overtime. So at five days a week…

- 8-hour workday: $28.85 hourly pay (almost $30 an hour pay scale)

- 10-hour workday: $23.08 hourly pay

Just because you make a $60,000 annual salary, you don’t take that amount home! You still have to pay taxes. Let’s look at how that impacts your take-home (after-tax) pay.

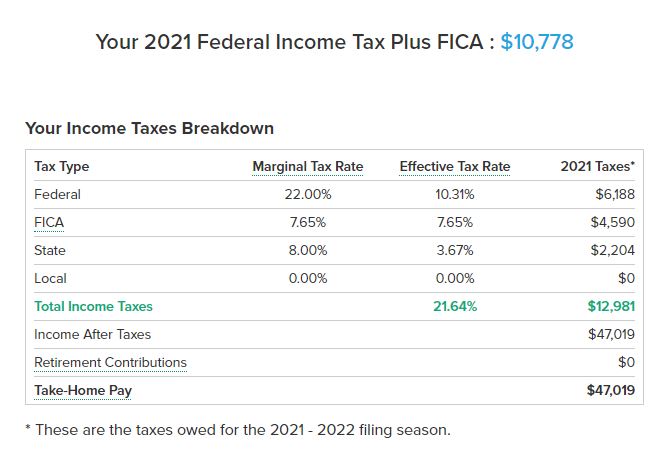

If you make a $60k salary, how much is that after federal and state taxes?

Figuring out your tax burden is vital to understanding your pay. You’re in for a nasty shock if you do the math and base your bills on before-tax income! So always consider how much you’ll pay in taxes.

For example, let’s assume you’re a single filer:

- If you live in California, which has a very high state income tax rate…

- You’ll pay $12,981 annually in FICA, federal and state taxes (roughly)

- You’ll take home $47,019 (before insurance and misc deductions)

You can go here to give you a rough idea of how much you’ll pay. Remember, this is just a reasonable rough estimate, not a guarantee! Or, if you want a super quick calculation, taking 25-30% off your gross is a good and safe estimate for this tax bracket. This percentage would include taxes, insurance & retirement contributions.

The current tax rate for $60k a year

If you make $60k a year and are single with no children, your current tax rate is 22% for federal taxes…

- $40,526 to $86,375 income = 22% tax rate

What do retirement contributions do to my take-home pay?

I am so glad you asked! Putting money into your employer-sponsored retirement plan is one of the smartest things for long-term financial planning! So yes, you absolutely want to do this!

Companies usually match a specific amount (as a percentage) of the pay that you put in. So if you put in 5% of your gross income into a traditional 401k, they will also match that 5%. Usually, companies have a max amount that they will contribute; 5% is a good general figure.

So, if you make $60,000 a year and contribute 5%, that means $3,000 annually in workplace retirement plan contributions by you and another $3,000 with your employer match!

You now have a taxable income of $57,000. Using the same calculator shown above, you’ll take home $44,919 (before insurance deductions).

- $47,019 take home with no retirement contributions

- $44,919 with a 5% contribution

- = a difference of $2,070 in take-home pay (before medical and other misc deductions).

The graph below shows what a 5% retirement contribution looks like plus a 5% company match over the span of 30 years. Don’t forget that you’ll probably get raises along the way too which will bump up your future total balance.

At the end of 30 years, at 7% return, you’ll have…

- Contributed $180,100 (total principal)

- Earned $343,349 in interest

- Total of $614,449

If you’re changing jobs, then you need to make sure that you take all your money with you! According to Capitalize, “As of May 2021, we estimate that there are 24.3 million forgotten 401(k)s holding approximately $1.35 trillion in assets, with another 2.8 million left behind.

That’s a lot of money for employees to just “forget about.” Don’t be a worker who left money on the table when they switched jobs! Beagle can help you find your old 401k accounts and help you roll them over into an account that you can easily manage.

While the full process takes a few days (they need 2-3 days to research everything), the initial sign-up process takes less than 15 minutes. You tell them your info, give them an idea of what companies you worked for, and they go find your old accounts.

We went through the process, and it was super easy; you can read our full review on Beagle retirement savings finder here! Or you can check out Beagle by clicking the green button below.

How much does insurance take from my $60,000 annual salary?

Sorry to say that we’re not done with your paycheck deductions. According to the U.S. Bureau of Labor, “Health care is typically one of the most expensive benefits for employers to provide, constituting 8.2 percent of total compensation for civilian workers in March 2020.”

It’s important to note the precedence of what get’s taken out of your paycheck and when. Here’s the order according to the U.S. Office of Human Resources…

- Retirement contributions come out first, followed by

- Social Security tax

- Medicare tax

- Federal income tax

- Health insurance

- Life insurance

- State income tax

- Local income tax

- Collections to the U.S. government (if applicable)

- Collections to Court ordered rulings (if applicable)

- *Everything below here is optional*

- Health Care/Limited-Expense Health Care Flexible Spending Accounts

- Dental

- Vision

- Health Savings Account

- Optional Life Insurance Premiums

- Long-Term Care Insurance Programs

- Dependent-Care Flexible Spending Accounts

- Thrift Savings Plan (TSP)

Did your jaw drop? It did for me; that’s a lot of deductions. Let’s concentrate on medical deductions and how they affect your earnings.

The situation is the same as in the above example, with a single filer making one deduction and living in California…

- $60,000 / 12 months = $5,000

- Minus 5% in retirement contributions $250 monthly

- Minus FICA, federal and state taxes = $1,007 a month

- Totals $3,743

- Minus 8.2% average medical insurance costs

- That takes out $307 leaving you with $3,436

- Minus misc small deduction averaging $100 (a total guess)

- = $3,336 net monthly income

This means roughly 33.3% of your paycheck is money you never see in your bank account.

| $60,000 a… | Before Taxes | After all Deductions |

|---|---|---|

| Year | $60,000 | $46,620 |

| Month | $5,000 | $3,336 |

| Bi-week | $2,308 | $1,793 |

| Week | $1,154 | $897 |

| Day | $231 | $179 |

| Hour | $28.85 | $22.42 |

How to live on $60k a year

People often warn about lifestyle creep when you get a big income jump. This can mean that you start spending more money, sometimes without realizing it.

To stick to a monthly take-home budget of $3,336, you need to be careful about your spending habits and ensure that all your expenses are accounted for. Here’s how to do it…

- Make a realistic monthly budget; here are the popular budgeting methods

- Save up for significant expenses (use sinking funds)

- Dump your debt ASAP (paying interest is eating away at your bank account, do it this way)

- Evaluate, Tweak & Adjust, and reanalyze (everyone needs to adjust, no one is perfect at budgeting)

- Live within your means (you have to say no to yourself sometimes). Let’s dive into this aspect more – The Joneses.

How should I budget a 60k salary?

Okay, let’s take the figures from above and figure out your monthly budget. So we’re using a take-home pay of $3,336 and giving figures for two popular budgeting methods.

The 50/30/20 budgeting method

This budgeting method is best for people who like flexibility and have leeway for spontaneity. They want general guidelines, but they want options & choices too. So your monthly household budget would look like this…

- 50% Needs: $1,668 for housing and utilities

- 30% Wants: $1,001 for wants

- 20% Savings: $667 for saving

Dave Ramsey recommended budget percentages

I am a fan of Dave’s budget percentages, but I realize that this method can be too detailed and constraining for some. However, others need to be told exact amounts to help them feel comfortable and secure.

Knowing norms is a good place to start with budgeting, but know that people continually tweak and adjust their numbers.

But let’s see what everything comes to…

- Housing 25%

- Insurance 10 – 25%

- Food 10-15%

- Giving 10%

- Saving 10%

- Transportation 10%

- Utilities 5-10%

- Health 5-10%

- Recreation 5-10%

- Personal Spending 5-10%

- Misc 5-10%

| Budget Category | Percentage | Amount |

|---|---|---|

| Housing | 25% | $834 |

| Insurance | 10 – 25% | $337 – $834 |

| Food | 10 – 15% | $337 – $500 |

| Giving | 10% | $337 |

| Saving | 10% | $337 |

| Transportation | 10% | $337 |

| Utilities | 5 – 10% | $167 – $337 |

| Health | 5 – 10% | $167 – $337 |

| Recreation | 5 – 10% | $167 – $337 |

| Personal | 5 – 10% | $167 – $337 |

| Misc | 5 – 10% | $167 – $337 |

Can you live off of $60k a year?

These numbers are not always a decent living wage if you live in a high cost of living area. Your housing and food expenses may be considerably higher than the budget category allowance allows, or vice versa in a low-cost of living region.

To add in another layer of difficulty, if you made $60K in a metro area, that same skill might only pay $45K in a more rural area, which can be frustrating.

According to the Bureau of Labor Statistics for May 2020, the average annual wage for a U.S. worker across all occupations is $56,310. So a $60K a year job is slightly higher than the average. HOWEVER, where you live plays a significant impact in if it’s considered a good wage.

For example, the BLS states that in NYC, the average yearly salary is $71,050. While in Idaho, the average salary is $46,800. But remember, a few people skew the numbers for these BLS averages.

A better number is the median wage; that’s the halfway point of the number of people. The BLS site shares info on the national median hourly wage being $20.07. Remember, with a 40 hr work week, that makes your $60k salary $28.85 an hour, so well above the median wage.

Another factor is your household annual income (as a whole), not just your income. So The U.S. Census says that in 2019 (the most recent data), the median household income is $62,843. So if you make $60,000 and your spouse makes $60,000, then at $120,000 total, you are doing great!

Is $60,000 a year salary good if you’re single?

If you’re single, your $60K salary is considered above average. You’re doing great. But remember, how much you make is only half of the equation; the other half is how much you keep (aka save).

Is $40k a good salary for a family?

A $60,000 salary may be enough for a family, depending on the size of the family and where they live. This salary could cover all of your expenses in a low-cost living area certainly.

But in a high cost of living area, this salary might be just enough to cover. Again, it all depends on your lifestyle. How careful you are with your money and how well you plan for the future.

Let’s go ahead and take a look at a few other typical salaries and see how they’d support your family’s needs.

- $30,000 a year is how much an hour

- $40,000 a year is how much an hour

- $50,000 a year is how much an hour

- $60,000 a year is how much an hour (you’re here)

- $70,000 a year is how much an hour

- $80,000 a year is how much an hour

- $90,000 a year is how much an hour

Jobs that make $60,000 a year

Many jobs make $60,000 a year; let’s look at Indeed’s list…

- Asset protection specialist – $60,177

- Instrument technician – $61,088

- Truck driver – $61,711

- Ranch manager – $63.339

- Cargo pilot – $64,667

- Sales rep – $65,155

- Electrical foreman – $67,473

What about bonuses?

It’s common for salaried employees to receive other paycheck perks, such as bonuses and profit-sharing plans. These are a common form of employee compensation.

Depending on the business, you may be eligible for a yearly or quarterly bonus. This is in addition to your regular income and is frequently given as a percentage of your pay. For example, if you earn $60,000 per year and get a

- $60,000 x 5% bonus = $3,000 (gross) x .70 taxes = $2,100 extra take home pay

- $60,000 x 10% bonus = $6,000 (gross) x .70 taxes = $4,200 extra take home pay

- $60,000 x 15% bonus = $9,000 (gross) x .70 taxes = $6,300 extra take home pay

Bonuses are frequently given when a company/department meets or exceeds a sales objective or achieves some sort of quota.

It’s also important to note that your bonus money may be taxed differently than your normal amount. It depends on how your company classifies it.

Bankrate states, “A bonus is always a welcome bump in pay, but it’s taxed differently from regular income. Instead of adding it to your ordinary income and taxing it at your top marginal tax rate, the IRS considers bonuses to be “supplemental wages” and levies a flat 22 percent federal withholding rate.”

$65,000 a year is how much an hour?

- $5,417 monthly salary

- $2,500 bi-weekly

- $1,250 a weekly income

- $250 a day

- $31.25 an hour (for 8 hr workday)

All figures are gross (before taxes).

At the end of the day

So, is a $60,000 job enough? The answer to that question really depends on your personal circumstances. If you have a lot of debt or expensive tastes, then it may not be enough for you and your family.

But if you’re comfortable with a modest standard of living (with a few splurges) and don’t have any pressing financial needs, then this pay could suit you and your family just fine.

Ultimately, only you can decide if a $60,000 annual salary is enough and is it worth the trade-off for the kind of work that pays this amount.

Q: How much is $60,000 a year per hour?

A: $28.85